Doprava zadarmo s Packetou nad 59.99 €

Pošta 4.49 €

SPS 4.99 €

Kuriér GLS 3.99 €

Zberné miesto GLS 2.99 €

Packeta kurýr 4.99 €

Packeta 2.99 €

SPS Parcel Shop 2.99 €

Ako nakupovať

Ako nakupovať

Pomoc

Doručenie

Pošta 4.49 €

SPS 4.99 €

Kuriér GLS 3.99 €

Zberné miesto GLS 2.99 €

Packeta kurýr 4.99 €

Packeta 2.99 €

SPS Parcel Shop 2.99 €

Doprava zadarmo s Packetou nad 59.99 €

Nákupný poradca

Sme tu pre Vás!

02/210 210 99

Môj účet

Staňte sa súčasťou komunity milovníkov kníh z celého sveta a získajte hromadu výhod.

Založiť účet zdarma

▸

Prázdny :-(

0

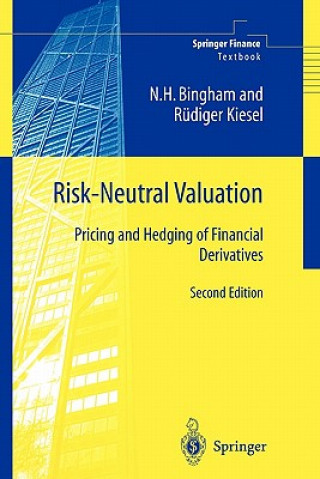

Risk-Neutral Valuation

Jazyk

Angličtina

Angličtina

Angličtina

Kniha

Brožovaná

This second edition - completely up to date with new exercises - provides a comprehensive and self-c...

Celý popis

Libristo kód: 01434764

?

195 b

195 b

195 b

77.48

€

Skladom u dodávateľa v malom množstve

Odosielame za 13-16 dní

30 dní na vrátenie tovaru

Mohlo by vás tiež zaujímať

/

List

/

List

11.76

€

11.76

€

This second edition - completely up to date with new exercises - provides a comprehensive and self-contained treatment of the probabilistic theory behind the risk-neutral valuation principle and its application to the pricing and hedging of financial derivatives. On the probabilistic side, both discrete- and continuous-time stochastic processes are treated, with special emphasis on martingale theory, stochastic integration and change-of-measure techniques. Based on firm probabilistic foundations, general properties of discrete- and continuous-time financial market models are discussed.

Informácie o knihe

Celý názov

Risk-Neutral Valuation

Jazyk

Angličtina

Angličtina

Väzba

Kniha - Brožovaná

Dátum vydania

2010

Počet strán

438

EAN

9781849968737

ISBN

184996873X

Libristo kód

01434764

Nakladateľstvo

Springer London Ltd

Váha

682

Rozmery

158 x 233 x 24