How to shop

How to shopDelivery

Shopping guide

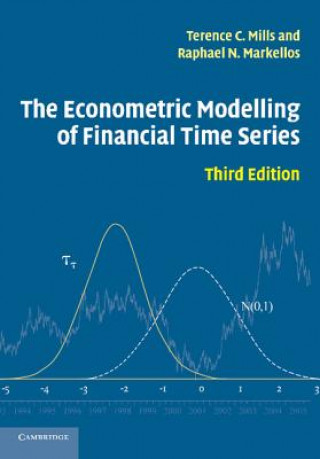

Econometric Modelling of Financial Time Series

English

English

173 b

173 b

30-day return policy

You might also be interested in

Terence Mills' best-selling graduate textbook provides detailed coverage of the latest research techniques and findings relating to the empirical analysis of financial markets. In its previous editions it has become required reading for many graduate courses on the econometrics of financial modelling. The third edition, co-authored with Raphael Markellos, contains a wealth of new material reflecting the developments of the last decade. Particular attention is paid to the wide range of nonlinear models that are used to analyse financial data observed at high frequencies and to the long memory characteristics found in financial time series. The central material on unit root processes and the modelling of trends and structural breaks has been substantially expanded into a chapter of its own. There is also an extended discussion of the treatment of volatility, accompanied by a new chapter on nonlinearity and its testing.

About the book

English